“If you can’t measure something, it’s difficult to improve it.“

Why Cash Flow Planning Matters

Most people budget by tracking expenses, but that’s only half the picture. Cash flow planning—planning inflows and outflows over time—gives you a dynamic view of your financial health so that you can make strategic decisions. Whether you’re:

- Planning to emigrate (where upfront costs can be steep),

- Saving for a home or investment,

- Or just avoiding paycheck-to-paycheck stress…

…understanding cash flow is the key. In this article, I am only talking about making a PLAN. The purpose of a plan is to understand your current situation and what your limits are. Tracking your expenses and setting a budget are separate exercises. It’ll be more clear when you reach the example.

Planning gives you strategic direction. Budgeting and tracking is about control.

Canadian Emigrant: I’ve always had a habit of looking at my cash flow plan at least once a quarter. This helps me to understand how much cash I can set aside for leisure vs investment spending.

Step 1: Map Your Cash Inflows

Recurring Income (Predictable):

- Employment income (salary/wages)

- Interest/dividends (investments)

- Rental income

- Side hustles or freelance work

In many countries, income tax is deducted from your payroll. When you file your taxes, you would know what your final tax burden should be and either have a refund or a tax payable. For simplicity, I suggest you do things on a “cash as received” basis. If you pay taxes quarterly, then factor in a tax payable in the month(s) you expect to pay tax. Conversely if you expect a tax refund in a given month, then put an estimate in that month. So for employment income, put your “take home pay”.

One-Time or Variable Income:

- Tax refunds

- Bonuses

- Asset sales (e.g., car, property)

- Gifts/inheritances

For things like bonuses, you might not know the performance of your company at the time you start your exercise. If you want to be absolutely conservative, you should put $0.

Step 2: Subtract Committed Expenses

These are non-negotiable, short-term obligations:

- Rent/mortgage

- Utilities (electricity, water, internet)

- Insurance (health, auto, home)

- Groceries

- Debt payments (student loans, credit cards)

- Transportation (gas, transit passes)

- Taxes

In Canada auto insurance is mandatory by law if you have a car and want to drive it. Home and health insurance are optional. Your country may have different rules and circumstances. Consider what expenses are inescapable and add to this section. In Asia for example, many people get around with public transit and auto insurance would not be at play.

While there are ways to “save” on groceries and utilities, ultimate you still need to put a number there unless you live with someone who takes care of all these.

Formula:

Disposable Income = Total Inflows – Committed Expenses

Step 3: Allocate Disposable Income Wisely

This is your flexible money—use it for:

- Lifestyle Spending:

- Travel

- Dining out

- Entertainment

- Future Goals:

- Investments (stocks, real estate)

- Emergency fund

- Big purchases (e.g., relocation fund, education)

Why Excel is the Perfect Tool for Cash Flow Planning

Because it’s simple, free, and flexible. Yes I’m sure there are software out there who can do all this for you. But this type of planning is not something you do every day. For tracking expenses and budgeting, yeah you can try to use an app. This exercise is Cash Flow Planning! Not budget and expense tracking.

The other reason you DON’T want to automate too much is because you actually want to take time to process through your brain. The part that’s helpful to automate is the math and Excel takes care of that for you. Everyone’s template is going to look different in terms of having different sources of inflows and outflows.

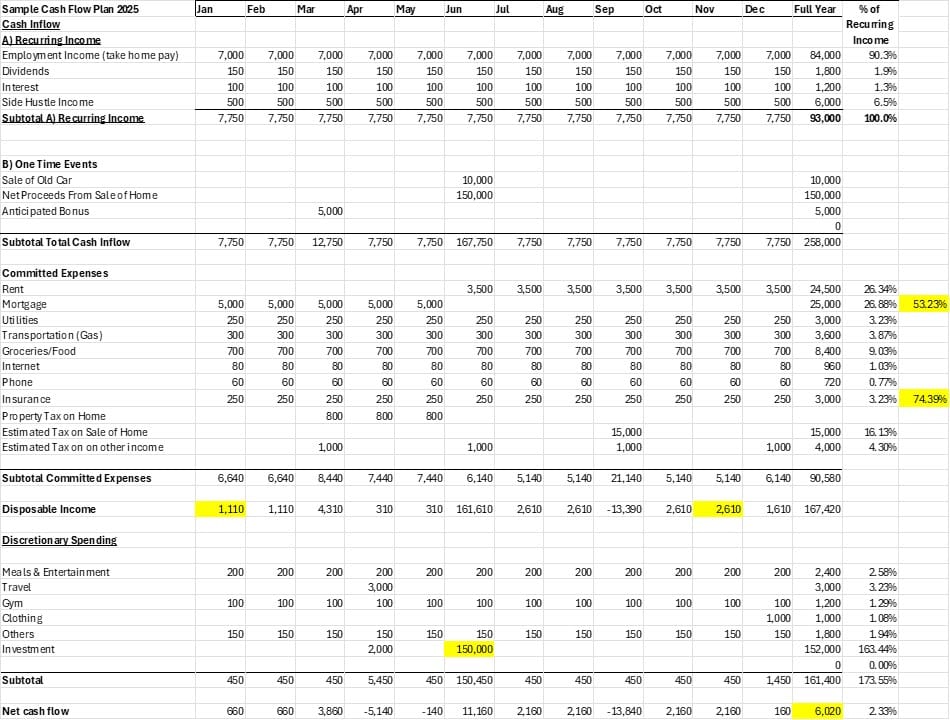

Here’s a sample cash flow plan. I recommend doing it by calendar year but you’re free to define your own time frame. I make one spreadsheet per calendar year. I want to emphasize simplicity and that’s why the template I use as example is so vanilla.

This article is getting long. I’ll do an example of a cash flow plan in a separate post and do some analysis. Read on for part 2.