What is Net Worth?

Imagine you were to sell all your assets and turn them into cash. At the same time, you need to settle all your debts. If, after liquidating all your assets and paying off your debts, you have a positive number, then you have a positive net worth.

In other words:

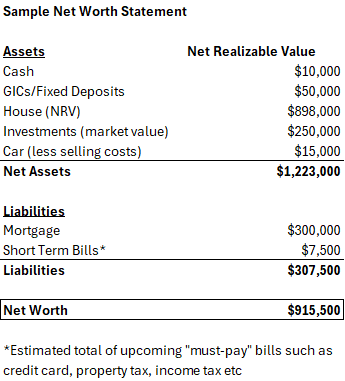

Net Worth = Assets minus Liabilities

More specifically, it’s the Net Realizable Value (NRV) of your assets minus your liabilities.

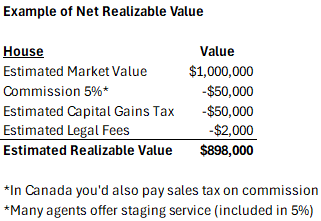

What does net realizable value mean? It’s similar to what accountants call Fair Market Value. Here’s an example to make it clear:

- You own a house and want to know its NRV.

- Start with a conservative estimate of what your house is worth based on market research (specific to your neighbourhood).

- Deduct estimated costs associated with selling the house, including taxes, commissions, and any other fees you can reasonably expect to incur.

If you think you need to do renovations, you could estimate the cost and factor it into the calculation. However, I recommend keeping it simple. Net worth is meant to be a snapshot of your financial situation today. You haven’t done the renovations yet, and whether they’re worth the cost is a separate analysis.

I said your net worth calculation should be a snapshot of your situation today. The capital gains tax might not be payable immediately upon the completion of the transaction. However, it is a guaranteed cost if you were to proceed with selling the house so you should include it. In the same way, commission is part of the transaction costs that you can’t avoid. Meanwhile, unless you deem renovations as mandatory, you do not need to include it.

Note that the amount you initially paid for the house is a sunk cost and doesn’t factor into your net worth calculation. However, it may matter when estimating your taxes, as you may need to report capital gains.

Also, net worth is generally just an estimate because many assets are only worth what a buyer is willing to pay. Until you sell the house, you won’t know its exact value. But for net worth calculations, such precision isn’t necessary. The goal is to create a simple snapshot of your wealth level. However, take a conservative approach—don’t be overly optimistic with your valuations.

Personally, I reexamine my net worth about once a quarter or whenever there’s a major change in my situation or the market. You can update it as frequently as you see fit, but calculating it more often doesn’t add much value.

Net worth calculation does not need to be an exact science. For example, if you typically don’t have a lot of short term bills such as credit card payments or property taxes, you can omit it altogether. The idea is to capture the big picture. However, you can be as precise as you want. It’s your finances!

If you need a more detailed discussion about assets and liabilities, refer to this article: Net Worth: What Assets and Liabilities to Include?

Why is Knowing Your Net Worth Important When Planning to Emigrate?

Most immigration processes will ask to see your assets and/or proof of income. Countries generally don’t accept immigrants who can’t contribute to society (except Canada, of course!). Nor do they want people who arrive and can’t sustain themselves.

Furthermore, many immigration processes require a minimum amount of cash that you need to bring into the country. If your net worth is tied up in assets, you’ll need to sell some of them to meet this requirement. Even if the country doesn’t specify a minimum cash requirement, you’ll want to know how long you can survive on your savings in case you fail to secure employment or other income sources.

Understanding your net worth is a good financial habit, even if you’re not planning to emigrate. For example: You did some research and concluded that it’ll cost $2M to do an early retirement in your target country. You’re at $1.5M now. Then you can work out much longer you need to work before you retire.

Knowing your finances can also help you make the big purchase decisions such as what kind of home you can afford to buy or what your monthly budget should be. I’ll cover cash flow budgeting in separate articles.

What are you waiting for? If you don’t have a net worth statement yet, open up an Excel spreadsheet and create one. You don’t need any fancy tools to get started. I know there exists some software out there that can do fancy visualizations and also track your expenses. Maybe I’m biased as an accountant, but I find Excel to be sufficient and highly flexible.