Let me put the sample up again and we’ll jump right into the key elements to think about. For an introduction to cash flow planning, click here.

Key Lessons From This Example

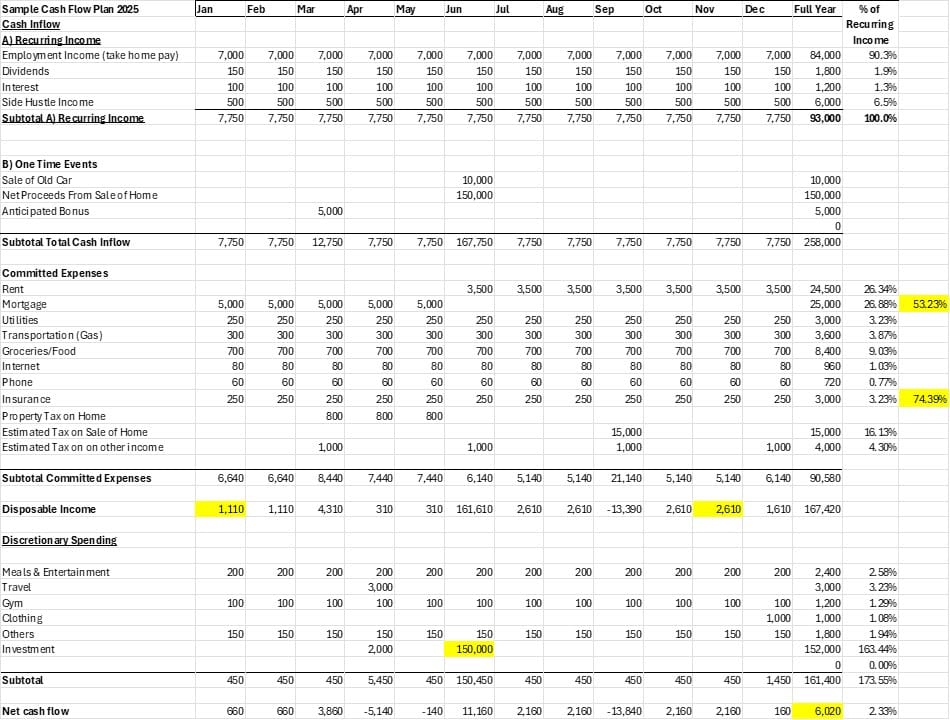

This template is very similar to my actual situation in 2024. In terms of income, I had a steady job with predictable monthly income and also an annual bonus. I had investments generating passive income. I didn’t have any side hustles (at that time) but I threw that in for illustration purposes. I had a home that I wanted to get rid of and then I would switch to renting until I left Canada.

This fictional person who is eerily similar to me had a home that he was planning to sell. This person also planned to downsize to one car instead of two so he expects extra cash inflow in the same month. Since this is a PLAN, you don’t know the actual proceeds from the sale. But as usual, I recommend you put in a conservative figure. Do some market research. You also don’t know the TIMING of the sale but let’s just say the closing of the home will be in June. Also to note on the sale of the house, this person has a mortgage. From the sales price, typically you should subtract: a) remaining mortgage balance b) commission c) estimated legal fees d) any land transfer taxes (usually borne by the buyer in Canada). In North America, typically you’d work with a lawyer and the lawyer will ensure each party gets their share. Note that you would not pay the capital gains tax until later so it’s important to account for that. In this example, let’s say the capital gains tax on the property is $15k and payable a few months later.

As an aside, in Canada if a property was your principal residence for the entire duration of ownership, you do not pay any capital gains tax but there are signals that this treatment may change.

Every country will have their own rules. In Canada where I used to live, commission is fully paid by the seller (typically deducted from the deposit). In Hong Kong where I live now, the going rate is 1% from both the buyer and the seller (total 2%). In Hong Kong the buyer also has to pay a stamp duty (that’s the name of the tax) and this is payable on signing a firm contract rather than payable on closing.

The committed expense section is rather self explanatory. The items listed are very commonly “inescapable” expenses such as groceries and utilities.

As you can see, a lot of the planning boils down to understanding the nuances of the rules applicable to your situation. The more you understand the market and the rules, the more precise your plan is. However…

Don’t Stress Too Much About Precision

Again, this whole cash planning exercise is meant to give you strategic direction. Some numbers can be highly exact like phone bills as your base plan fee might only change once a year. For utilities, you can probably put in a reasonably good estimate. Some things like the sale of the house would be more fuzzy. Many people have an emotional attachment to their house and may have an inflated sense of its worth.

Strategically, this is what the above sample plan is saying about your calendar year:

- As long as I have my job, and before I sell my house, I have roughly $1100 of disposable income per month that I can spend on leisure or investments

- After I sell the house, my disposable income is roughly $2600 per month assuming I keep my job and I find a suitable place to rent which I expect to cost $3500 per month.

- Selling the house will generate a big whack of cash and I plan to invest most of it, leaving a little behind to pay taxes.

- I’ve planned out some of my major optional spending such as $1000 for Boxing Day shopping (December) and I plan to spend $3000 to travel somewhere, probably in April.

- If you combine rent and mortgage payments, I’m spending about 53% of my recurring take home pay on housing.

- Housing + other necessities add up to almost 75% of my recurring disposable income. The anticipated sale of my home is a one time transaction. So in a “normal” year I’m able to save about 25% of my recurring normal income.

- Note that the net cash flow for the entire year is still positive. Around $6000. This gives you a bit of a cushion in case you want to spend more on other things. There’s no need to “zero-out”. You can always decide to invest more into the stock market or spend more once the uncertain items have played out.

- Some months will have negative cash flow and that is often ok. You should always have some emergency cash and have your spare cash earning interest in a savings account. A negative month just means you are dipping into your savings.

Framework For Thinking About Disposable Income

When thinking about disposable income, it’s important to separate one time events from recurring. In this example, you can see that while this person has a mortgage to pay, his disposable income in a “normal” month is only about $1100. After he switches to renting where he no longer needs to pay a mortgage but has to pay rent instead, his disposable income is $2600. Having made a plan like this puts your life in a better perspective. You know roughly how much you can afford to spend on leisure activities and/or investments per month.

But the above is not to say we don’t consider one time events at all. The sale of the home obviously will generate a significant amount of cash. It would be wise to put the money to work…perhaps into the stock market. So you can see that in the same month as the anticipated sale of the house, $140k is planned under “investments”. But note that it’s not the full $150k of proceeds because you need to reserve $15k for the tax man. If you have other debts like student loans or auto loan, then making a cash flow plan is going to help you make better decisions. You probably want to pay off any outstanding loans from the $150k before investing the money.

You can also work backwards and work out your budget when looking for a place to rent. For example, given your other “hard” committed expenses, and after considering your investment and travel plans, what is the most you should spend on rent?

Living Pay Cheque To Pay Cheque? Negative Disposable Income?

You are probably not alone. In America, studies have shown that many people can’t even come up with $400 USD in case of an emergency. Canadians are in a similar situation. Planning is the first step to helping you get out of the rut.

If your disposable income is not positive, then you have some soul searching to do. In a high cost of living country like Canada, you may find that your after tax income (“take home pay”) doesn’t even cover the cost of living. In fact, many fresh immigrants in recent years have found that after coming to Canada, they are dipping into their life savings because their after tax income isn’t sufficient. I’ve heard horror stories of people coming from developing countries who were at least able to save money in their home country.

Emigration could be one solution if you’re finding that your skills are not a match in the job market, or if the opportunities for entrepreneurship are non-existent. Or at least get a second passport and/or residency in another place to expand your options. If you can’t change the inflow side of the cash flow equation, perhaps you can emigrate to somewhere with a lower cost of living instead. But of course, you need to do your homework and consider what your income prospects are in the new target country. Unless you’re already half way to retirement with plentiful savings.

While having negative disposable income is undesirable, if you have significant savings, then it may not be an urgent issue. Negative disposable income just means you need to dip into your savings to survive. But this may be normal if you are a retiree for example. Not many people in the world can live purely from passive income.

Planning Doesn’t Limit Your Options. It Expands Them

The point of making a plan isn’t to set your life in stone. It’s to put your finances into perspective. For example, while you plan for a $3000 vacation in April, maybe your company doesn’t let you take leave that month or you find that your target destination would have expensive plane tickets in April due to a labor strike. So maybe as information changes, you can push back the vacation to later. Or perhaps you later estimate that the vacation will actually cost $5000 because you want to do this and that. Well, because you’ve made a plan, you know that you COULD afford to spend $2000 more but at the expense of having a little less to invest. The important thing is, you’ve factored in a vacation into your plan and it’s not a “surprise” item.

Vacation is a big item and for most people it deserves special attention. When it comes to smaller ticket items like dining out, I don’t bother with individual dining events. I just set a rough budget per month. In this example I set my monthly meals/entertainment budget at $200 which healthily lets you eat out once in a while.

I’ve met many people who absolutely loathe following a plan. Let me tell you something…the vast majority of them are not financial successful and never will be. They might find short periods in their life where they achieve success, but in the broader scheme of things, it’s always better to make a plan.